Commentary

China’s SOE Reforms: What the Latest Round of Reforms Mean for the Market

Written by: Zoey Ye Zhang, Asia Briefing, Dezan Shira & Associates

The latest round of China’s SOE reforms covers topics like “SOE classification”, “capital assets management”, “mixed ownership reform”, and “Party leadership”. China Briefing looks at these developments to help you understand how they might impact the market.

The reform of Chinese state-owned and state-holding enterprises (SOEs) has taken place for over four decades. It remains the core element of China’s economic reform process, but the official thinking regarding how they should be implemented has changed over time.

Since China’s SOEs are some of the biggest players in both the domestic and international markets, it is essential for foreign investors to gauge the strategic shifts brought about through the latest round of reforms.

This article discusses China’s SOE reform process, current policies, and what they mean for the market.

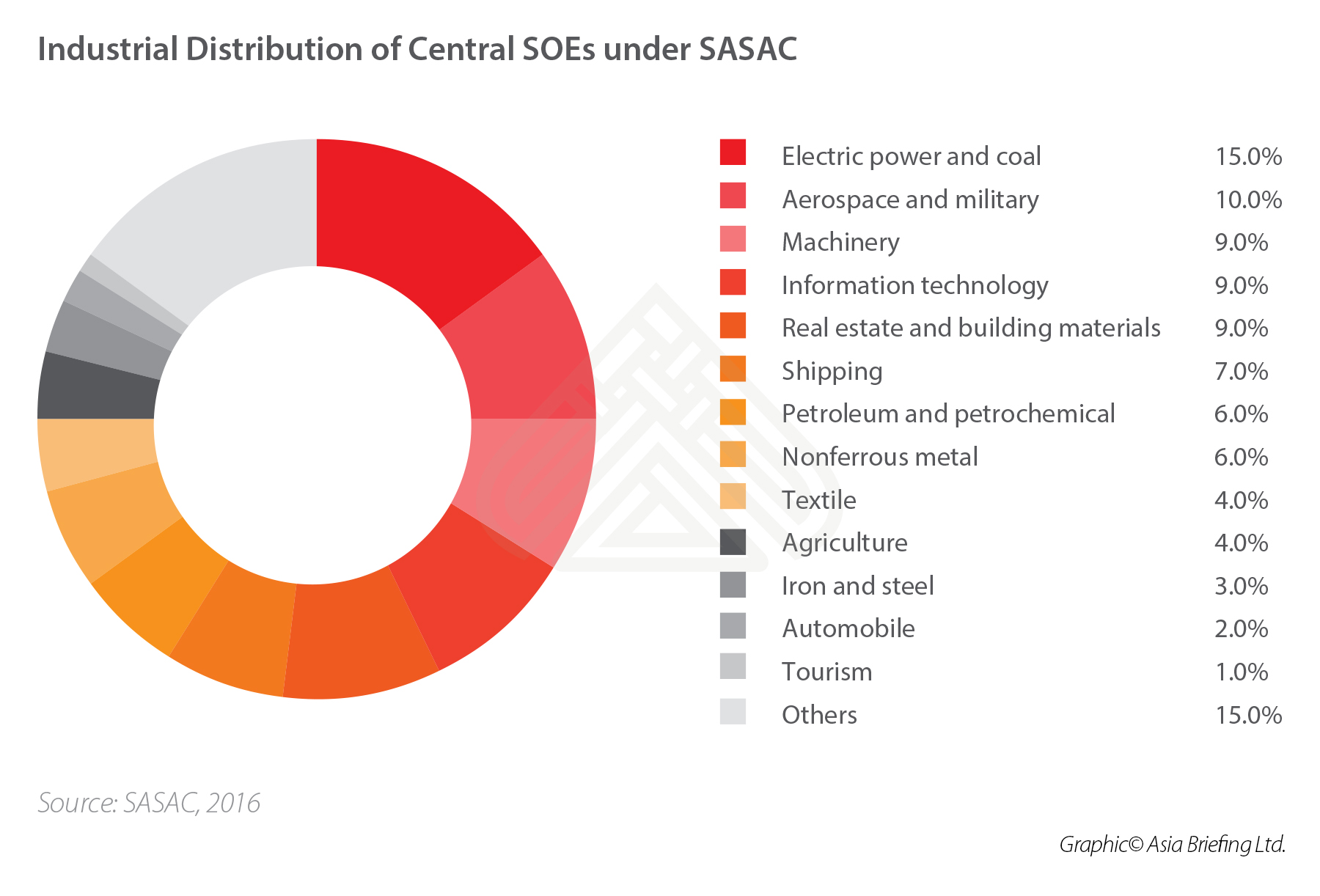

SOEs in China

Chinese SOEs contribute to around 30 percent of the country’s GDP. The proportion far exceeds that of developed countries.

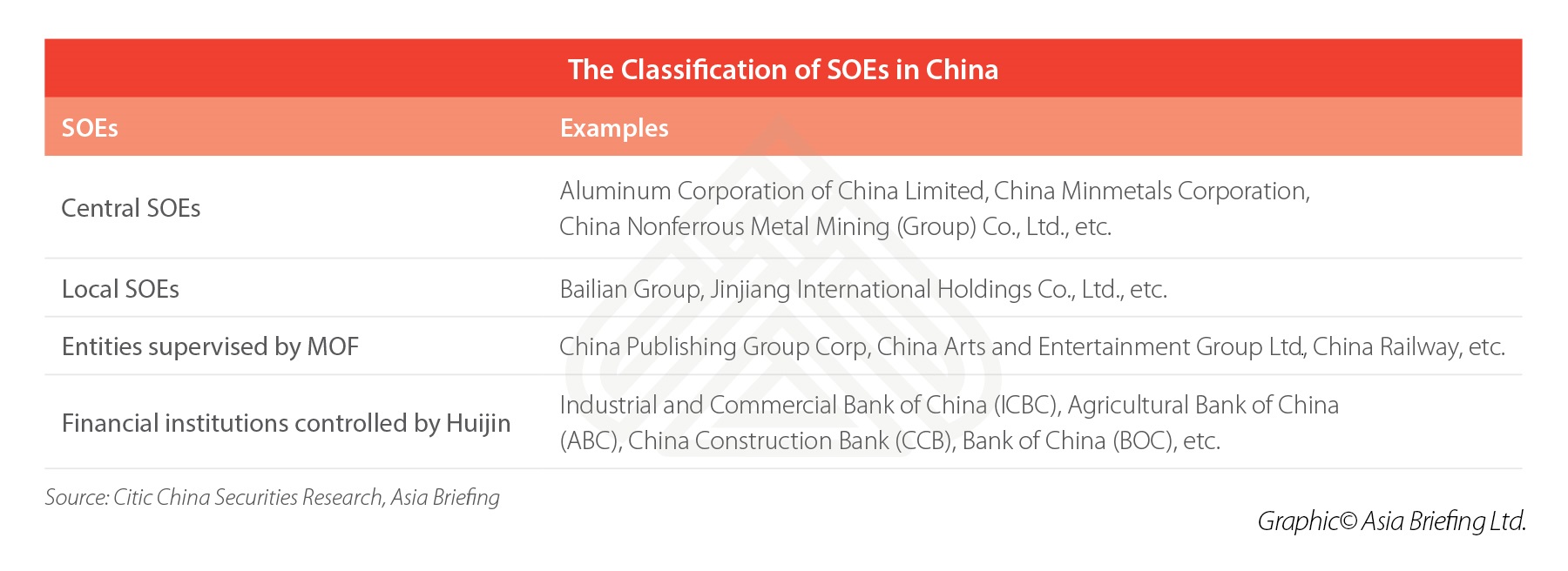

SOEs in China can be divided into four groups based on their regulators:

- Central industrial SOEs supervised by the central SASAC;

- Local industrial SOEs supervised by local SASACs;

- Financial institutions controlled by Central Huijin Investment Co., Ltd (Huijin); and

- Entities supervised by the Ministry of Finance (MOF).

Central and local industrial SOEs are overseen by the State-owned Assets Supervision and Administration Commission of the State Council (SASAC), a special commission directly under the State Council.

State-owned financial institutions are usually controlled by the Central Huijin Investment Co., Ltd (Huijin), an investment company owned by the Chinese government.

Besides these, the Ministry of Finance (MOF) also regulates some enterprises subordinate to central administrative institutions, some financial enterprises, and the SOEs having financial relations with MOF.

Central and local SOEs account for around 40 percent of the total number of enterprises. They are the main targets of this round of SOE reform, especially those in electricity, oil and gas, and railway industries.

State capital is mostly located in industries considered to be the lifeblood of the national economy – coal, nonferrous metals, steel, electricity, and construction industries. Some of these, however, have been the hardest hit by overcapacity.

Multiple reasons account for why SOEs do not function efficiently and are seen elsewhere as a drag on the economy. In the case of China, unclear property rights between the government and enterprises and laggard company management systems mean that SOEs are generally not as productive and innovative as private firms. Consequently, many suffer from over-capacity and debt.

According to research by the Rhodium Group, a consultancy firm, as of June 2018, the average return on assets among SOEs was 3.9 percent, compared with 9.9 percent for private firms. They accounted for 28 percent of China’s industrial assets but contributed to only 18 percent of the total profit. Further, they racked up RMB 100 trillion (US$15 trillion) in debt by the end of 2017, equivalent to 120 percent of the national GDP.

SOE reforms in China: A short history

While it is recognized that SOEs should be more marketized to boost their productivity in the long run, the Chinese government instead focuses on how to balance the commercial and political objectives of its SOEs.

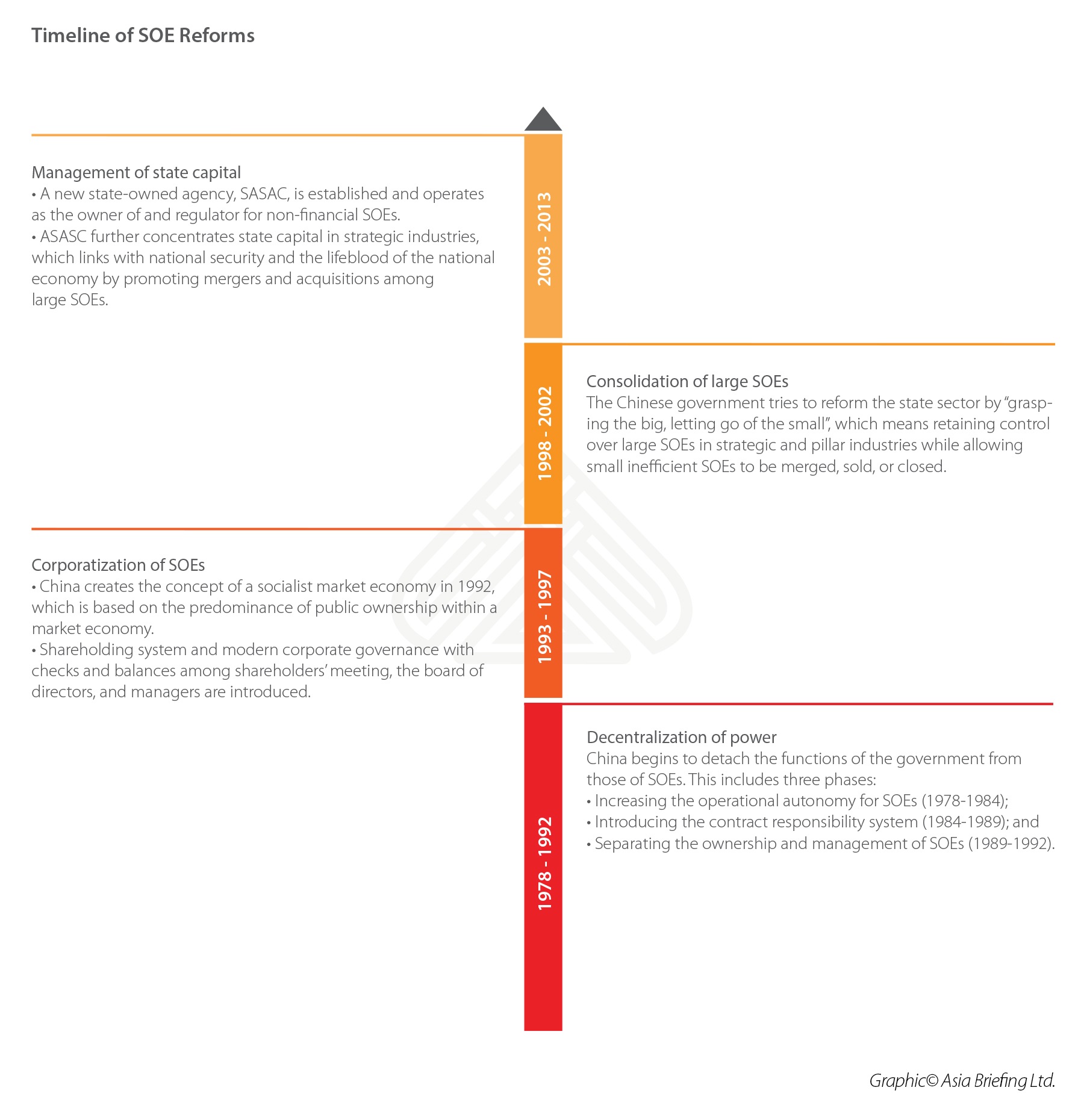

China’s SOE reforms have gone through several stages over the last 40 years.

From the 1970s to 1990s, SOEs were state-controlled factories, who were directly controlled by the governments to accomplish the state-assigned production quotas; gradually these entities were converted to become modern corporates.

Since the late 1990s, large SOEs have gone through mergers and reorganization but remain the dominant type of entity in strategic industries.

In 2003, the SASAC was set up to act as the funder and regulator of non-financial SOEs on behalf of the state. In 2006, the Chinese leadership divided industries into three groups and readjusted the allocation of state assets. The thinking being that state-owned assets should maintain absolute control over key industries that are vital to national security and the lifeblood of the national economy, maintain strong control over in pillar industries, which has strategic linkage to national economic development, and maintain the necessary influence in normal industries.

- Key industries: Defense, electricity, oil and gas, telecom, coal, shipping, aviation, and rail.

- Pillar industries: Auto, chemicals, construction, electronics, equipment manufacturing, nonferrous metals, prospecting, steel, and technology.

- Normal industries: Agriculture, pharmaceutical, real estate, tourism, investment, professional services, general trade, and general manufacturing.

The more recent stage of reforms began in 2013, when President Xi Jinping outlined his ambitious reform plans at the Third Plenum meeting.

Consistent with previous policies, the meeting reemphasized the transformation of SOEs into modern corporations by introducing mixed ownership, hiring professional managers, establishing boards of directors, and authorizing them to make market decisions.

Xi also proposed to shift the role of the government from the management of state enterprises to the management of state capital. This meant that the government could allocate state capital towards strategic industries while reducing direct intervention within the day-to-day operations of SOEs.

In 2015, a major SOE reform policy document, the Guiding Opinions of the Central Committee and State Council on Deepening the Reform of SOEs, was released and elaborated on familiar messages from the 2013 plans. However, the document classified SOEs as “public class” and “commercial class”. Different types of SOEs were to have different supervision mechanisms, mixed ownership reform plans, and corporate governance mechanisms, etc.

But these opinions no longer mentioned the “decisive role for markets in resource allocation”. It seemed that, following China’s 2015 stock market turmoil, the leadership in Beijing was reluctant to withdraw the “visible hand” of the state. Today, the government’s agenda for SOE reforms combines SOE corporate governance with the institutionalization of Party leadership within SOEs.

Currently, the predominant view is that Chinese SOEs should lead the country’s economic and technology catch-up.

At the 19th National Congress of the Communist Party of China, Xi pledged further reforms to make SOEs “stronger, better, and bigger,” and turn them into “world-class, globally competitive firms.” In 2018, 48 central SOEs made the list of Global Fortune 500 – the same number as in 2017, but up from only six in 2003.

This sparked controversy and debate both at home and abroad.

Internationally, the US accused the Chinese government of implementing policies that directly favored SOEs thereby distorting the allocation of market resources and disrupting the level playing field. Domestically, public opinion asserted that as the Chinese state advanced, the private sector retreated.

In response to the disquiet over the direction of SOE reform, national leaders and officials proposed to treat SOEs with the governing principle of “competitive neutrality”.

This year’s government work report stated that “when it comes to access to factors of production, market access and licenses, business operations, government procurement, public biddings, and so on, enterprises under all forms of ownership will be treated on an equal footing”.

Current SOE reform policies

Following the 2015 policy document, a series of policy papers were released until 2017 and constituted the framework for the current SOE reform, also referred to as the “1+N framework”. We think there are three points worth paying attention to in this round of SOE reforms.

Mixed ownership

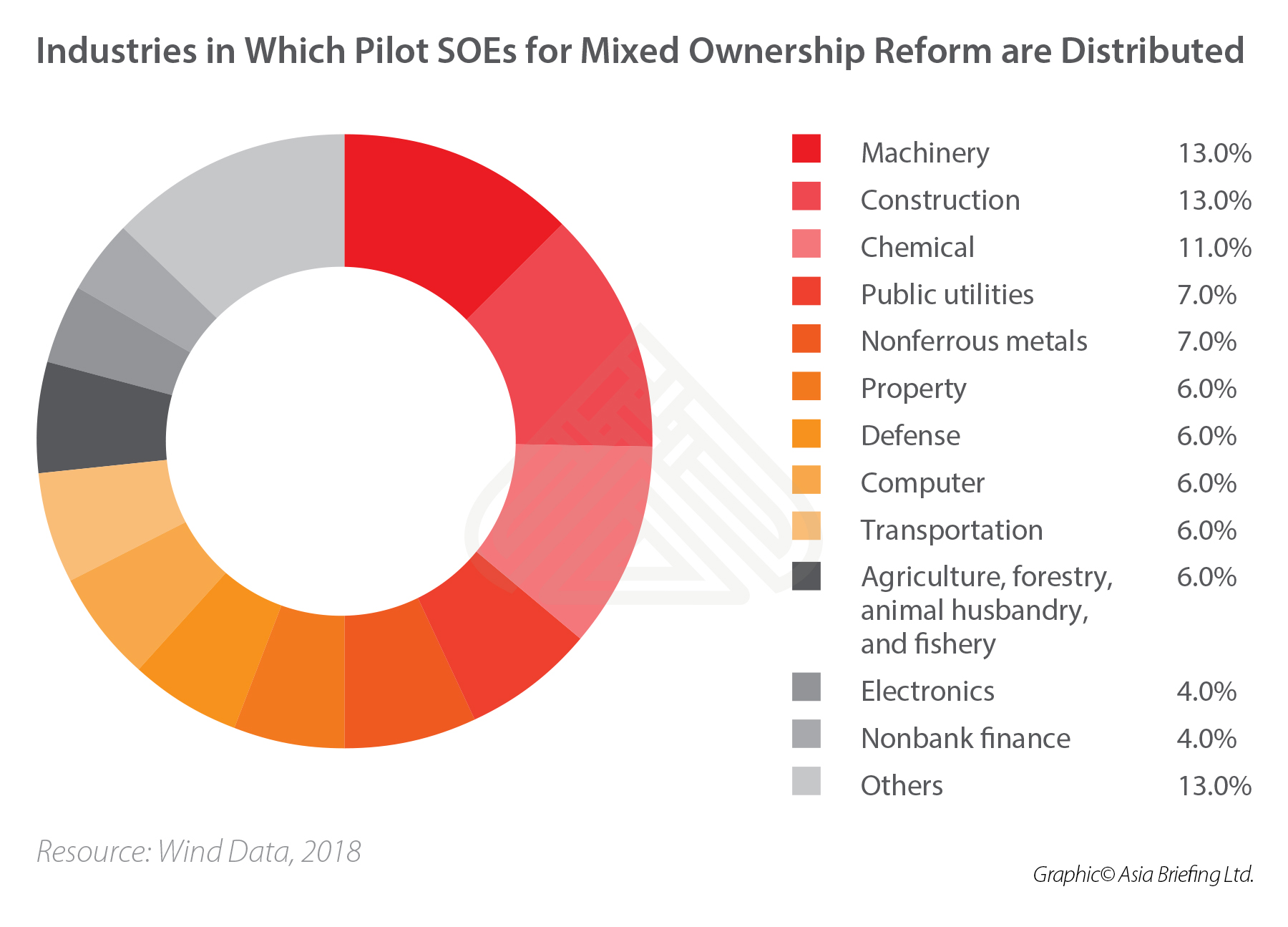

In August 2018, SASAC launched the “Double hundred action” work plan for SOE reform, aiming to add a total of 404 pilot subsidiaries of central SOEs and local SOEs into the mixed ownership reform pilot program during the 2018-2020 period.

According to Wind, a leading Chinese financial data provider, the selected pilot central and local SOEs are mainly in competitive industries and industries with excess capacity, such as machinery, construction, chemical, nonferrous metals, and more.

Pilot SOEs are required to actively introduce various investors to realize equity diversification through different means, such as restructuring and public listing.

Until the end of 2018, three batches of pilot SOEs, totaling 50 enterprises, had joined the mixed ownership reform plan. The list of the fourth batch of over 100 enterprises is about to be confirmed and will impact more industries in 2019.

Merger and acquisition

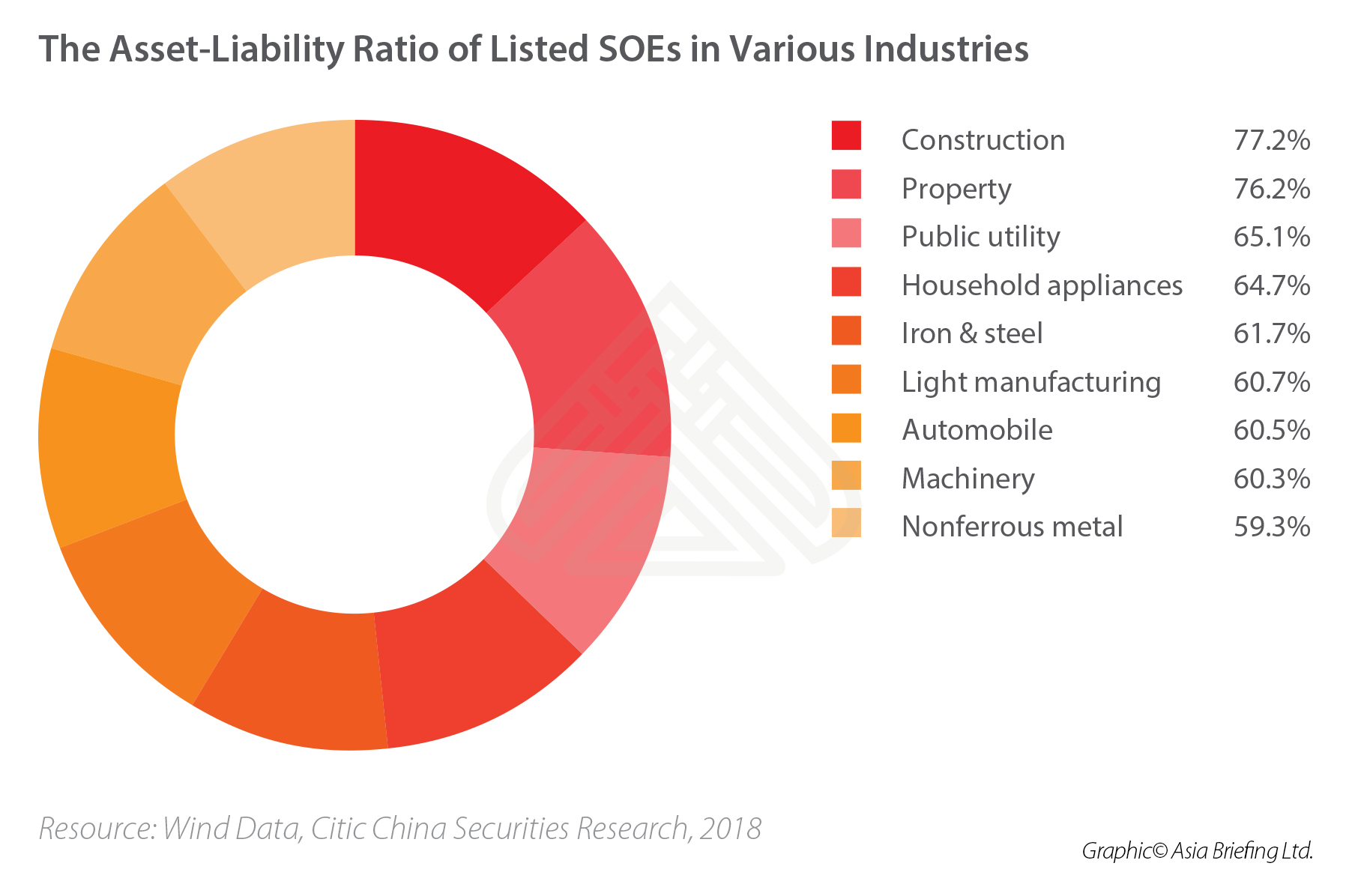

Through mergers and reorganization, SOE groups can improve the asset securitization rate by injecting unlisted assets into listed companies. Listed companies can improve the structure of assets and liabilities and achieve the reduction of leverage by acquiring external high-quality assets.

According to data from Wind, industry-wise, SOEs in construction, property, public utility, household appliances, and iron and steel have a high asset-liability ratio.

In 2018, mergers and acquisitions of SOEs took place in highly leveraged industries, such as property, public utilities, chemical, machinery, and more. In the future, there may still be more M&A and restructuring opportunities for SOEs in related industries.

SOE classification and state capital management

In 2015, the leadership in Beijing intended to classify SOEs into a “public class” or “commercial class” as the basis for a new round of SOE reform. In 2017, the original binary categories were updated to a tripartite grouping scheme – industrial enterprises groups, investment groups, and operating groups.

In this way, the government and SASACs no longer directly manage state-owned groups, but only manage state-owned investment groups and operating groups. In turn, the state-owned investment groups and operating groups will manage individual enterprises in the way of “managing capital”, to reduce direct state interference in SOE commercial activities.

China’s SOE reforms are ambitious, but traditional fault lines remain

Mixed ownership reform, SOE M&As, and the establishment of “two types of companies” – investment groups and operating groups – are features of the latest reforms of SOEs in various industries and regions across China.

According to data from SASAC, until the end of 2018, more than two-thirds of all subsidiaries under central SOEs had achieved mixed ownership. Pilot enterprises introduced 40 investors of various types with capital exceeding RMB 90 billion (US$13.5 billion). The main industries involved are: electricity, oil and gas, railway, iron and steel, nonferrous metal, coal, and construction. Region-wise – Shandong, Shanxi, Tianjin, Zhejiang, Liaoning, and Guangzhou – are at the forefront of promoting “mixed reform” efforts.

In 2018, referring to the mixed ownership reform, Shandong launched mixed projects for 93 local SOEs focusing on infrastructure and public services. Tianjin launched 232 projects involving real estate, manufacturing, finance, services, and other fields.

Shanxi launched 108 projects involving manufacturing, power, energy, and other fields. Liaoning launched 48 projects involving steel, automobile, coal, energy, and other fields. Zhejiang launched 40 projects involving transportation, energy, environmental protection, and other fields. Guangzhou promoted 20 projects involving scientific and technological innovation, commerce, finance and other fields, according to SASAC.

Reports found that in 2019, SASAC and the National Development and Reform Commission (NDRC) reemphasized SOE reforms, especially the mixed ownership reform. As the list of more than 100 pilot SOEs for mixed ownership reform has been preliminarily confirmed, 2019 could see broader SOE reforms in the fields of equipment manufacturing, shipping, chemical industry, electricity, non-ferrous metals, steel and iron, and environmental protection.

But to be noted, although the central leadership alleged to protect the interests of all types of investors who participated in the mixed-ownership reform of SOEs, private investors and international actors may have limited capacity to directly influence Chinese policy-making or even SOE governance at the group company level.

Examples like the 2017 restructuring of China’s Unicom’s Shanghai-listed flagship subsidiary showed that private investors likely own a low average percentage (around three percent) of company shares and remain weak players on the board of directors.

Besides this, the creation of larger and more complex SOEs and the emphasis of “party leadership” raises worries among domestic private and foreign investors alike. Data from Bloomberg and the Rhodium Group show that from 2016, the share of SOEs in listed company revenues began to show a minimum decline in the least strategic industries. The concerns about the retreating private sector are growing. For this, last November, President Xi Jinping made two widely publicized speeches praising private enterprises and assuring them of official support.

The current, highly publicized move to open up China ostensibly seeks to achieve a more level playing field in the market but traditional fault lines remain as Xi stresses on assured political control in all sectors and decision-making areas.

It seems that the latest round of China’s SOE reforms, as previously, will only be gradual instead of at one stroke

This article was first published by China Briefing, which is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia from offices across the world, including in in China, Hong Kong, Vietnam, Singapore, India, and Russia. Readers may write info@dezshira.com for more support.